Want to Lower Your Medicare Premium? It Pays to Plan Ahead!

Updated JANUARY 29, 2026

Many seniors breathe a sigh of relief upon reaching age 65—and qualifying for Medicare. Private health insurance is a major household expense for those aged 50-64, and Medicare coverage is significantly cheaper. Even so, some seniors are surprised to learn that they could be subject to additional out-of-pocket Medicare premiums (often called a “Medicare Stealth Tax”) if their Modified Adjusted Gross Income (MAGI) exceeds certain breakpoints. Medicare assesses an “Income-Related Monthly Adjustment Amount” (IRMAA)—essentially a surcharge for higher-income retirees. Depending on household income, this annual surcharge adds between $974 and $5,844 per beneficiary:

Understanding Medicare’s Income-Related Premium Adjustments

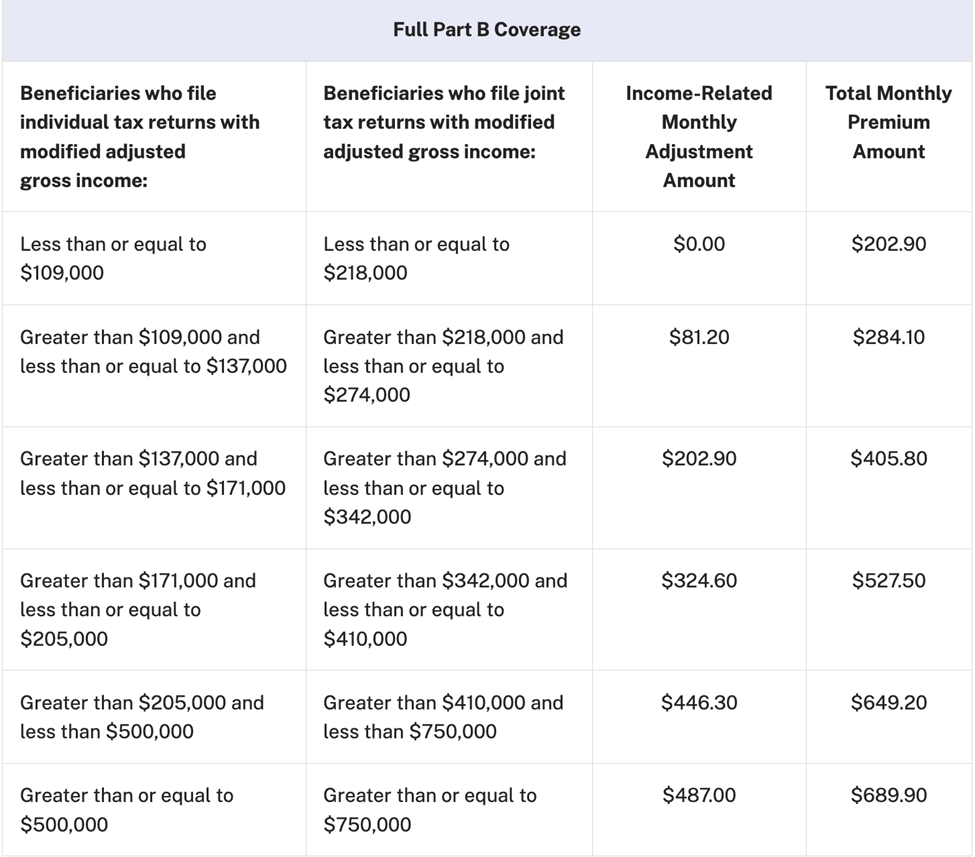

Source: Centers for Medicare & Medicaid Services

Source: Centers for Medicare & Medicaid Services

The table above summarizes the IRMAA surcharge for 2026. Importantly, IRMAA applies if MAGI is even $1 above the breakpoints outlined above. Further complicating matters, IRMAA is calculated on a two-year lag. This means that the IRMAA for 2026 is calculated based on an enrollee’s 2024 Modified Adjusted Gross Income. Therefore, even people who are two years away from Medicare enrollment could be setting themselves up for an IRMAA surcharge, if their income is skewed higher by one-time items such as the sale of a property or business. Among the many other age-related milestones that are important to retirement planning, wealthy seniors should scrutinize their annual income beginning in the year they turn 63.

Wealthy Retirees are More Vulnerable to the Medicare “Stealth Tax”

While fewer than 10% of Medicare enrollees are subject to IRMAA, those with large investment portfolios are more likely to be impacted since their income can fluctuate widely from year to year (due to timing of realized capital gains, or commencement of required minimum distributions from IRA accounts). Therefore, Medicare enrollees on the cusp of an IRMAA breakpoint may want to limit discretionary investment income in order to avoid triggering this additional charge.

4 Ways to Lower Your MAGI…and Your Medicare Premium

What are some ways to limit discretionary investment income, particularly later in the year?

- Postpone Capital Gains: To the extent that investors have discretion on the timing of asset sales in taxable accounts, pushing them a few months back (into the subsequent tax year) can keep MAGI below a critical breakpoint.

- “Harvest” Capital Losses: Similarly, selling assets with an unrealized loss pulls forward a capital loss which can be used to offset capital gains realized earlier in the year. Moreover, if total realized losses exceed total realized gains, up to $3,000 per year of these net capital losses can be deducted against ordinary income (further reducing MAGI).

- Maximize Deductions: While the 2017 Tax Reform raised the standard deduction (and reduced the value of certain itemized deductions), those who are charitably inclined can still benefit from itemization by bunching contributions (particularly in-kind contributions of appreciated stock) in alternating tax years. For example, a couple who typically donate $2,000 per year to charity could instead make a one-time donation of $20,000 to a donor-advised fund, which would allow them to immediately itemize the deduction in the current tax year, while dispensing the funds gradually to their desired charities over many subsequent years. Additionally, seniors who are still working can avail themselves of more generous “catch-up” contributions limits to company-sponsored retirement accounts, which may reduce MAGI in the years immediately preceding retirement.

- Consider a QCD: Another charitable option for investors aged 70 1/2 and above is a Qualified Charitable Distribution (QCD). A QCD allows the IRA holder to satisfy their required minimum distribution (up to $110K in 2026, indexed to inflation thereafter) by sending funds directly from their IRA account to a qualified charity. Unlike a regular RMD, the QCD is not counted as taxable income for the IRA account holder. Moreover, a QCD does not require the taxpayer to itemize deductions (i.e., if they would otherwise benefit from a larger standard deduction).

Even with an IRMAA surcharge, Medicare is still a fantastic value for seniors. But the Medicare “Stealth Tax” is just one of many potential pitfalls in the tax code that a qualified, tax-conscious investment advisor can help mitigate.

Learn more about the ways that Bristlecone can optimize your portfolio’s tax-efficiency over time

Book a Free Consultation Today:

One of Bristlecone Value Partners’ principles is to communicate frequently, openly and honestly. We believe that our clients benefit from understanding our investment philosophy and process. Our views and opinions regarding investment prospects are "forward looking statements," which may or may not be accurate over the long term. While we believe we have a reasonable basis for our appraisals, and we have confidence in our opinions, actual results may differ materially from those we anticipate. Information provided in this blog should not be considered as a recommendation to purchase or sell any particular security. You can identify forward looking statements by words like "believe," "expect," "anticipate," or similar expressions when discussing particular portfolio holdings. We cannot assure future results and achievements. You should not place undue reliance on forward looking statements, which speak only as of the date of the blog entry. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Our comments are intended to reflect trading activity in a mature, unrestricted portfolio and might not be representative of actual activity in all portfolios. Portfolio holdings are subject to change without notice. Current and future performance may be lower or higher than the performance quoted in this blog.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and returns do not reflect the deduction of advisory fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase.

Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there can be no assurance that a portfolio will match or outperform any particular index or benchmark. Past Performance is not indicative of future results. All investment strategies have the potential for profit or loss; changes in investment strategies, contributions or withdrawals may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio.