Third Quarter 2025 Commentary: What Is Going On?

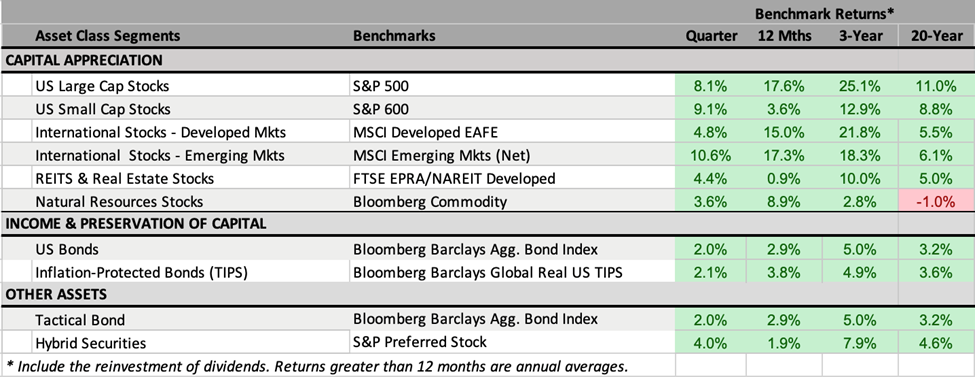

The third quarter produced strong results across all major asset classes. Stocks of all sizes and geographies performed well, and bonds also delivered solid returns.

Before zooming in further on key developments in this recent quarter, we're struck by just how much some things have changed in the markets and the economy over the last three years. A review across several fronts contextualizes the broader investment narrative, with this quarter being just the latest chapter.

The title of our third quarter 2022 commentary was "Finding the Bottom." Then, we were in the midst of a sharp downturn in the stock market, with the S&P 500 down 24% in the first 9 months of 2022. Sharply rising interest rates created one of the worst bear markets for bonds of all time (the Barclays Aggregate index of intermediate-term, investment-grade bonds was down 13% in 2022), reflecting a rapidly worsening inflation picture. The Russian invasion of Ukraine in February 2022 was a material rupture in the global geopolitical status quo.

Rising out of that hot mess of 2022, the subsequent 3 years were: 1) better than many expected economically (economic growth has been moderate and there was no recession despite many predictions); 2) well above average for stock returns (look at the 3-year column in the above table); and 3) surprisingly stable for interest rates. The Fed was well into its tightening regime in November 2022 when it made a 0.75% increase to a target Fed Funds rate of 3.75% - 4.0%, just below where it sits today. The rate on 10-year US Treasuries is almost exactly where it was in October 2022 - 4.0%, albeit with meaningful fluctuations along the way.

Without a doubt, the most significant development explaining the trajectory of the stock market over the last 3 years was the public introduction of ChatGPT in November 2022. This was a massive event on its own - ChatGPT became the fastest-growing consumer software application in history. It also introduced a new leading technology company, OpenAI. Most importantly, the introduction of ChatGPT crystallized a vision for the potential of AI in the minds of consumers, investors, and competitors around the world. In doing so, ChatGPT catalyzed an AI investment boom of astonishing scale and speed.

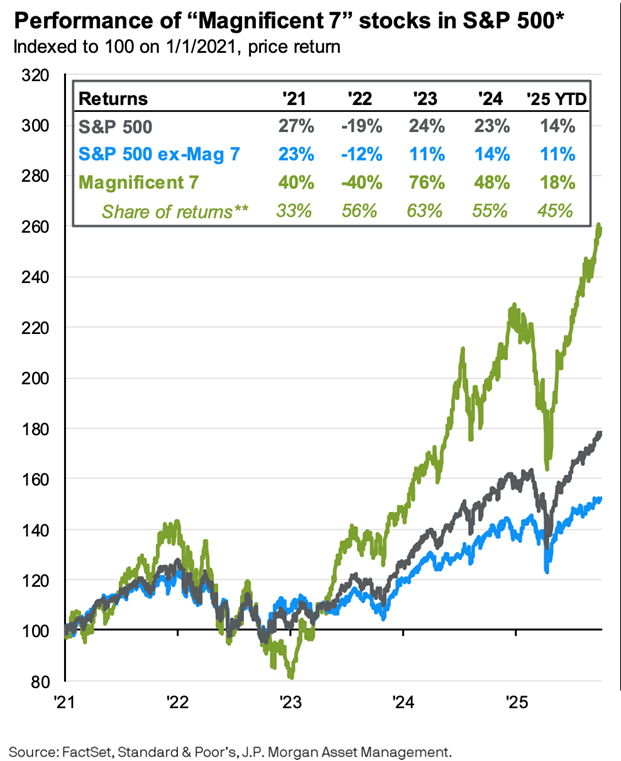

To the question of why the S&P 500 has done so well recently, we need look no further than the Magnificent 7. We use that moniker as shorthand, recognizing both that the seven are exposed to AI to quite varying degrees and also that there are other important companies beyond the seven participating (including OpenAI, which is still not publicly traded). This array of companies is making massive investments in AI infrastructure. Investors are rewarding them handsomely with higher valuations, and the cumulative market success of these companies means they now comprise a record large portion of the market (the largest ten companies in the S&P 500--all but two of them technology companies--made up more than 40% of the index weight at quarter end).

We will attempt to offer a little perspective below on whether this AI investment boom is going too far, too fast.

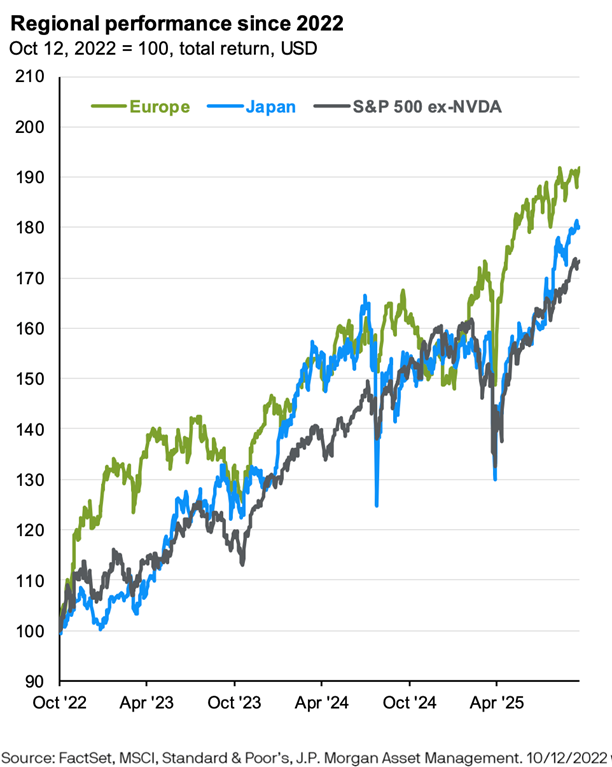

A second major theme for the quarter (and the last three years, really) is the re-emergence of international stocks. We've discussed this in all of our commentaries this year. However, it still may come as a shock to some that non-US stocks are finally delivering excellent returns after a long period of underperformance (essentially the period since the Great Financial Crisis running through the pandemic years).

There is no single explanation for this turn of fortune. After decades of poor stock market returns following the 1980s bubble, Japan introduced corporate governance reforms intended to improve shareholder value. Through listing incentives, a requirement for published value improvement plans, and even an effort to "name and shame" poor stewards of capital, corporate Japan is making tangible progress in improving returns on investments.

There are also significant pockets of innovation in Europe. ASML Holding, a Dutch company that makes semiconductor manufacturing equipment essential for building the most advanced chips, is now the largest company in the developed markets index (but still less than 10% the size of Nvidia, whose AI chips could not be made without ASML's technology). Danish company Novo Nordisk is one of the innovators and beneficiaries of the GLP-1 class of weight loss drugs.

We believe the larger explanation goes back to the relentless way in which capital seeks out higher returns. The gap in valuations between US stocks and the rest of the world just became too great for investors to ignore.

Bubblicious

Speculation is ever-present in markets, but it ebbs and flows in reaction to the broader investment environment. Today, there is much debate as to whether the boom in AI constitutes a bubble. Grounding our thinking more in our understanding of market and economic history rather than any special technical understanding of AI's potential, there are a few valuable contributions we can make to the conversation.

First, it's always important to distinguish the utility of a particular technological development from its investment merit. Whether analyzing railroads in the 19th century, the deployment of fiber optic cables in the 2000s, the broader internet boom, or AI today, there is usually a genuine reason for the excitement around the technologies. Most investment booms do hold the possibility for a positive economic impact.

In evaluating investment merit, rather than economic impact or technological potential, we strive to base our assessments on the simple equation for return on investment. That is: how much return (or profit) can we reasonably expect, divided by the amount of investment (or capital) required.

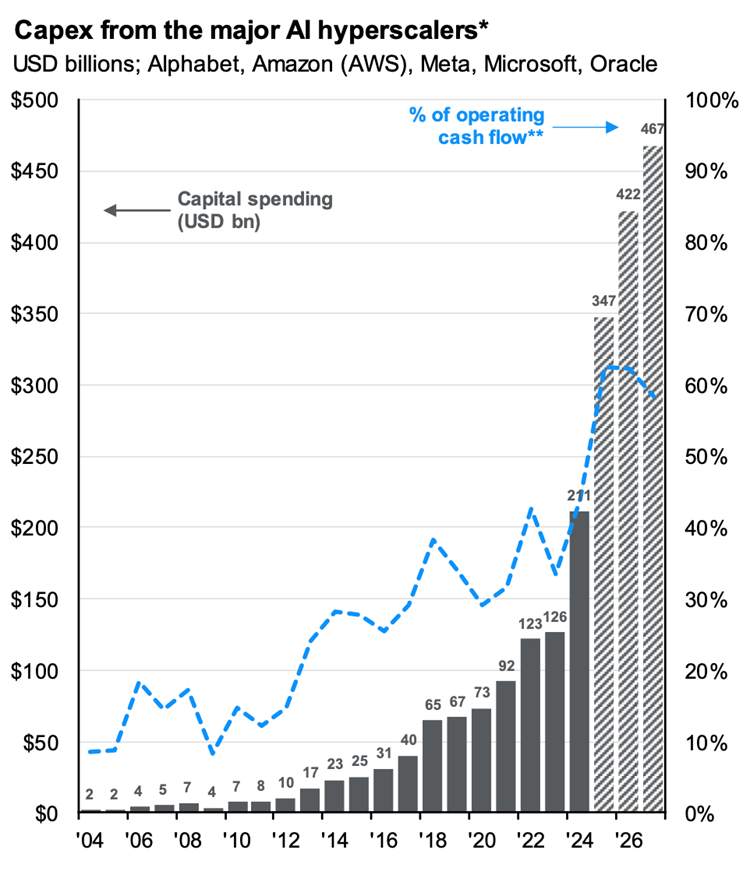

Source: J.P. Morgan Asset Management, Bloomberg

According to Bloomberg, OpenAI has recently "struck AI computing deals with Nvidia, AMD and Oracle Corp. that altogether could easily top $1 trillion." Setting aside that OpenAI is expected to have less than $15 billion in revenue this year (still an amazing figure!), and that they expect to remain unprofitable through the end of the decade, we are left pondering how realistic it is to expect the scale of profits necessary to earn a high return on that massive investment.

Companies like Alphabet, Apple, Meta, and Microsoft became exceptional because they were able to build globally scaled, very high-profit-margin businesses on relatively modest amounts of capital investment. With the recent explosion of investment in AI computing - whether in the form of data centers, the chips that perform the data processing, the human intellectual capital to design the software, or the mundane, but very critical, issue of generating the necessary electricity - it is becoming increasingly clear any future profits to these companies will come only after a comparatively massive amount of capital invested.

With a much, much larger denominator, the odds of earning a return on investment that justifies their current valuations are much lower.

Like most major technological advances, to truly succeed, the benefits of the technology need to be widely spread and valuable to a range of industries and consumers outside of the innovators themselves. This opens the possibility, maybe even the likelihood, that the benefits of AI advancements will ultimately be enjoyed far beyond the select group of early big-spending innovators in the spotlight today.

How To Invest Now

In that third quarter 2022 commentary, we ended with the question: What should thoughtful long-term investors do now? Then, we were conjuring some optimism amid a bleak landscape. Now, it seems appropriate to preach a small amount of caution in a much more ebullient market.

There are currently plenty of signs of speculative fervor. Non-cash producing assets (gold, silver, trading cards, cryptocurrencies) are hitting major new highs. Gambling is more popular than ever. The scale and structure of some of these AI investments are perplexing. There is a push to make private equity and other previously institutional-only investments available to individual investors. We believe none of these things is necessary to deliver the returns you need to meet your investment objectives.

While the last few years delivered great returns for stocks, and even though we believe long-term stock returns will surely be lower than these recent returns, we still believe a well-diversified portfolio of cash producing investments - stocks of profitable businesses around the world and high quality bonds that now promise a decent rate of interest and return of principal - will be able meet your investment objectives. Emphasizing global diversification and the importance of rebalancing (from lower expected return investments into higher expected return investments) seems more prudent than ever.

We are not predicting a recession or market crash -- only acknowledging that they will happen at some point, though their timing is impossible to know. We've endured a long and hard-earned education in the differences between investment and speculation, and those are the lessons we’ll assiduously seek to employ in managing your assets. As ever, we appreciate your confidence in Bristlecone.

One of Bristlecone Value Partners’ principles is to communicate frequently, openly and honestly. We believe that our clients benefit from understanding our investment philosophy and the process behind it. Our views and opinions regarding investment prospects are "forward-looking statements," which may or may not be accurate over the long term. While we believe we have a reasonable basis for our appraisals and confidence in our opinions, actual results may differ materially from those we anticipate. Information provided in this blog should not be considered as a recommendation to purchase or sell any particular security. You can identify forward-looking statements by words like "believe," "expect," "anticipate," or similar expressions when discussing particular portfolio holdings. We cannot assure future results and achievements. You should not place undue reliance on forward-looking statements, which speak only as of the date of the blog entry. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Our comments are intended to reflect trading activity in a mature, unrestricted portfolio and might not be representative of actual activity in all portfolios. Portfolio holdings are subject to change without notice. Current and future performance may be lower or higher than the performance quoted in this blog. References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest directly in an index, and returns do not account for the deduction of advisory fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase. Economic factors, market conditions, and investment strategies will affect the performance of any portfolio, and there can be no assurance that a portfolio will match or outperform any particular index or benchmark. Past Performance is not indicative of future results. All investment strategies carry the potential for profit or loss. Changes in investment strategies, contributions, or withdrawals can materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio. This content is developed from sources believed to provide accurate information, and it may not be used to avoid any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information and should not be considered a solicitation for the purchase or sale of any security.