Third Quarter 2020 – All in the FAAAM-ily

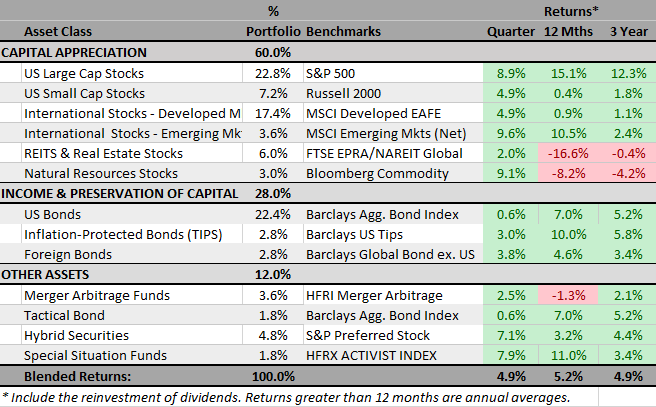

Global markets continued their recovery in the third quarter, albeit at a more measured pace than the second quarter. Once again, every major asset class notched positive returns, with stocks from Emerging Markets and Natural Resources leading the way. On the bond side, we note the excellent returns from US TIPS over the past 12 months, supported by lower interest rates and a change in inflation expectations. Finally, the other assets category performed well with average returns exceeding U.S. bonds' but lagging equities' overall.

Concentrated Leadership in U.S. Stocks

After dropping 34% between February 19th and March 23rd (the fastest bear market on record), the S&P 500 index subsequently rallied to a new all-time high by early September and finished the quarter up 50% from its March low (and +5.6% YTD). With corporate earnings estimates revised lower due to the pandemic, the S&P 500 trades at a higher multiple of expected earnings today than it has at any point since the technology bubble at the turn of the century:

Source: Charles Schwab

Although very low-interest rates largely support current high valuations for stocks, we remain justifiably cautious about prospective returns for stocks, mainly if inflation were to rise.

In our Q4 2019 commentary, we discussed how the S&P 500 had become increasingly top-heavy. At that time, the top 5 stocks in the index (by market capitalization) comprised 17% of the total. Fast forward nine months and the "FAAAM" cohort (Facebook, Apple, Amazon, Alphabet, and Microsoft) is approximately 23% of the index. If you were to exclude those five stocks from the S&P 500, its year-to-date return would be negative:

Source: Charles Schwab

A Policy Shift from the Fed

In late August, the U.S. Federal Reserve announced a significant policy shift that has implications for both stock and bond markets going forward. Historically, the Fed has balanced two mandates that are often in opposition: low inflation, and full employment. However, after several years of below-target inflation, and with unemployment still well above target due to the Covid-19 pandemic's dislocations, Fed governors indicated a more patient "average inflation targeting" policy. Essentially, they signaled a willingness to tolerate "above trend" inflation for some time to compensate for several years of below-target price increases. All of this points to interest rates remaining lower for longer—and perhaps a higher degree of inflation uncertainty as well.

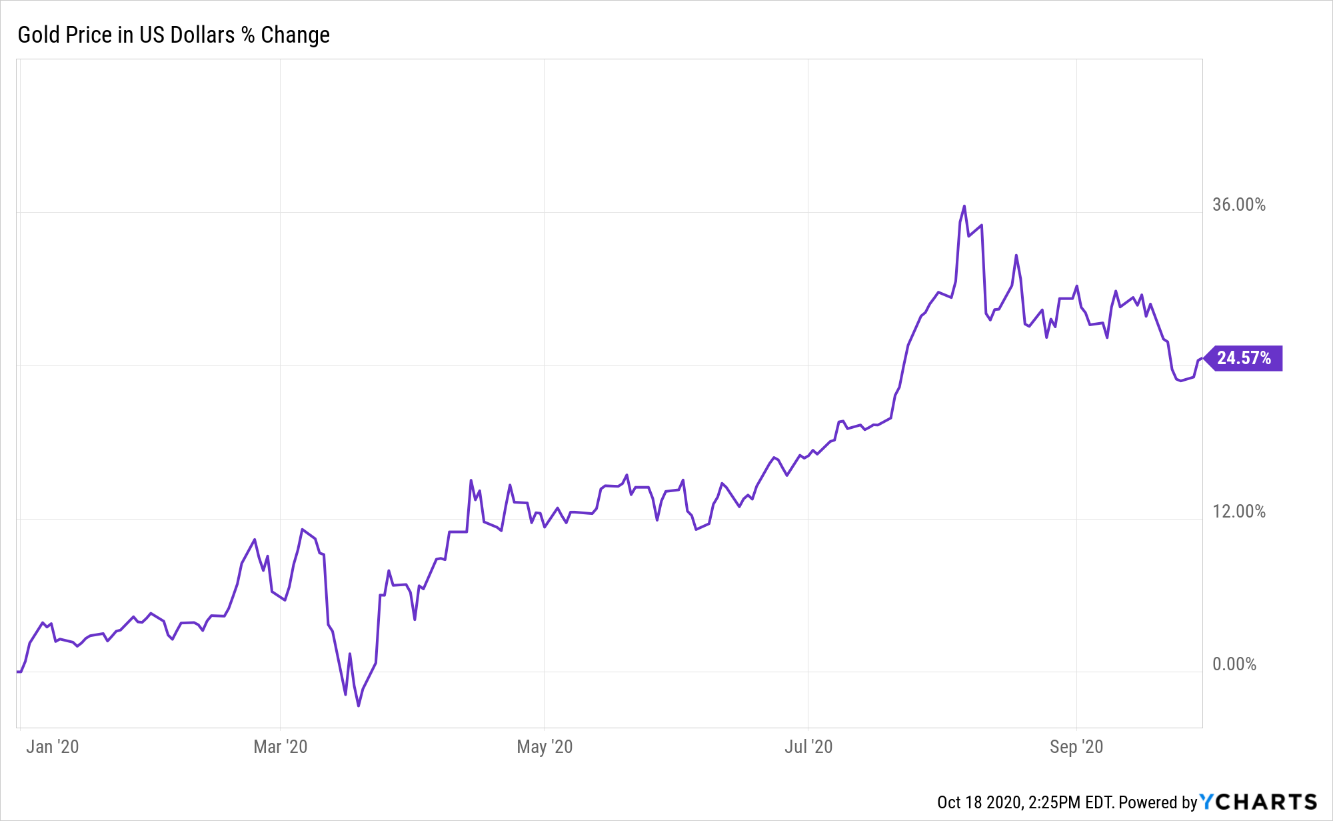

The Fed’s more permissive stance toward inflation, set against the backdrop of a surging Federal deficit tied to Coronavirus relief spending, propelled the price of gold to a new record high in August (the prior high was in August 2011. The monetary metal is up nearly 25% in the first nine months of 2020, reflecting some skepticism over the U.S. dollar’s status as a global reserve currency (the U.S. dollar index is down 2.7% through the first nine months of 2020, and 8.7% below its peak in late March).

Similarly, inflation-protected treasuries (TIPS) have outperformed most fixed income sectors this year, gaining 3% in Q3 and more than 9% YTD.

Lurking Risks in Passive Fixed Income

The secular decline in interest rates over the past few decades has been a tailwind for bond returns. Paradoxically, this has helped boost investor demand for bonds even as real yields (and future return expectations) have declined to almost nothing. As part of its extraordinary market interventions in late March, the Fed pledged that it would buy corporate debt—even from issuers subsequently downgraded to “junk” status—to support credit markets during the pandemic. This intervention bolstered investor confidence in corporate bonds, bidding up prices for the asset class (and driving down yields).

For their part, corporate borrowers responded to low rates and healthy investor demand by increasing their debt offerings' size and length to lock in attractive financing costs. To take one extreme example: Apple (AAPL), with nearly $200 billion in cash and investments on its balance sheet, nevertheless seized the opportunity to issue $5.5 billion in new debt in August, at yields ranging from 0.55% for a 5-year bond to 2.55% for a 40-year bond.

By early September 2020, U.S. corporate debt issuance exceeded $1.9 trillion, eclipsing the prior record for a full year. Moreover, within investment grade bond market, average duration (a measure of sensitivity to interest rates) is higher today than in the last 30 years.

Source: JP Morgan Guide to the Markets, 9/30/20

Thus, at the point where yields have diminished about as low as they can go, passive investors in corporate debt (i.e., through indexed ETFs and mutual funds) are exposed to more interest rate risk than they have been historically. No matter how you slice it, all bond investors will likely struggle to achieve appreciable real returns over the coming decade. However, we believe that active bond managers—who can target alpha from superior credit analysis while limiting duration risk—should be in a better position to outperform the aggregate bond market index. For this reason, we’ve begun the process of shifting the remainder of our passive taxable fixed income exposure into low-cost, actively managed funds.

Covid’s Winners & Losers

The Covid-19 pandemic disrupted virtually every business to some extent. Nearly all have had to adapt to new logistical impediments, regulatory restrictions, or novel kinks in their supply chain.

For example, early in the pandemic, stay-at-home orders led to shortages of toilet paper. Many instinctively blamed hoarders. However, the real explanation was more straightforward: the toilet paper supply chain is segmented into commercial and retail channels, each with distinct product specifications. When stay-at-home orders went into effect, customer demand went from being evenly distributed between these two channels to being heavily concentrated in the retail channel. In the short-term, this led to a retail shortage, even while there was an excess supply of commercial rolls (to the point where many businesses began giving away spare rolls as promotional items). More recently, industries as varied as aluminum cans and turkey farming have been upended by pandemic-related shifts in consumer behavior.

In short, social distancing requirements have spawned a new set of winners and losers for the market to sort out. In general, companies with a low debt burden, flexible overhead costs, and an ability to adapt quickly to changing consumer tastes have fared better. On the other hand, highly levered companies, or those reliant on physical customer traffic have struggled. Looking at year-to-date equity returns by sector bears this out: share prices for online retail and home improvement companies surged, while energy, travel, and physical retail suffered along with flagging demand for these companies’ products and services.

It is important to remember that this too shall pass. Although equity markets will continue to react sharply to news about infection rates and fatalities, the pandemic won’t last forever. Some industries will take longer to recover, but as the much more lethal 1918 Spanish flu outbreak demonstrates, the world will eventually return to normal.

Large-Cap Value (LCV) Review

(Not all clients of Bristlecone are invested in our Large-Cap Value Equity portfolio strategy, depending on the size of the overall portfolio and the client’s objectives and constraints.)

The average LCV portfolio modestly outperformed the S&P 500's 8.9% return in the third quarter yet trails the index year-to-date. The LCV portfolio is relatively under-weight the largest technology stocks that have driven returns for the S&P 500 so far this year while being relatively overweight to the financial sector, which has lagged. For the quarter, top performance contributors included AGCO Corp (AGCO), Hanesbrands (HBI), and Weyerhaeuser (WY). The biggest detractors were Bayer (BAYRY), Micro Focus International (MFGP), and Intel (INTC).

It was a quiet quarter for trading, as a rebounding market provided fewer opportunities to add to shares at incrementally attractive prices. One exception was Intel (INTC), which announced record Q2 sales in late July (up 19% year-over-year). Management raised their sales and earnings guidance for the full year, but also warned that the rollout of the firm’s next-generation chip technology would be delayed by an additional six months. The market reacted very negatively to the chip delay news, and the stock dropped about 20% within a week of the release. We took this opportunity to increase our investment in Intel, a long-term holding for the portfolio (since 2006), which we have variously increased or reduced at least 10 times in the intervening years, as valuation warranted.

A Word on Elections

The 2020 elections are shaping up to be the most contentious in recent memory, and early indications are that voter turnout (%) may reach levels not seen in several decades. Moreover, the preponderance of mail-in votes increases the likelihood that some races will not be decided until after Nov 3rd.

Clients on both sides of the political spectrum have voiced concerns about what might happen to financial markets if their preferred candidate doesn’t win. In the short-term, the answer is anybody’s guess. But those concerned about short-term volatility should keep in mind that it works both ways—the best and worst individual days for stock returns tend to occur in close succession. Moreover, there’s a large observed gap between stump proposals and implemented policy—the gears of government have a way of grinding down rough edges and moderating the most extreme impulses from either side.

The data is clearer in the long run: U.S. businesses have adapted and thrived under both Republican and Democratic administrations, through wars, natural disasters, terrorist attacks, and even pandemics. It's not timing the market that matters, but time in the market.

One of Bristlecone Value Partners’ principles is to communicate frequently, openly and honestly. We believe that our clients benefit from understanding our investment philosophy and process. Our views and opinions regarding investment prospects are "forward looking statements," which may or may not be accurate over the long term. While we believe we have a reasonable basis for our appraisals, and we have confidence in our opinions, actual results may differ materially from those we anticipate. Information provided in this blog should not be considered as a recommendation to purchase or sell any particular security. You can identify forward looking statements by words like "believe," "expect," "anticipate," or similar expressions when discussing particular portfolio holdings. We cannot assure future results and achievements. You should not place undue reliance on forward looking statements, which speak only as of the date of the blog entry. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Our comments are intended to reflect trading activity in a mature, unrestricted portfolio and might not be representative of actual activity in all portfolios. Portfolio holdings are subject to change without notice. Current and future performance may be lower or higher than the performance quoted in this blog.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and returns do not reflect the deduction of advisory fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase.

Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there can be no assurance that a portfolio will match or outperform any particular index or benchmark. Past Performance is not indicative of future results. All investment strategies have the potential for profit or loss; changes in investment strategies, contributions or withdrawals may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio.

This content is developed from sources believed to be providing accurate information, and it may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.