2020 in Review: The Beginning of the End?

2020 was a uniquely harrowing year. More than 1.7 million people have died in the COVID-19 pandemic, with trillions of dollars in economic damages around the world. Millions of people are out of work and struggling to pay their bills.

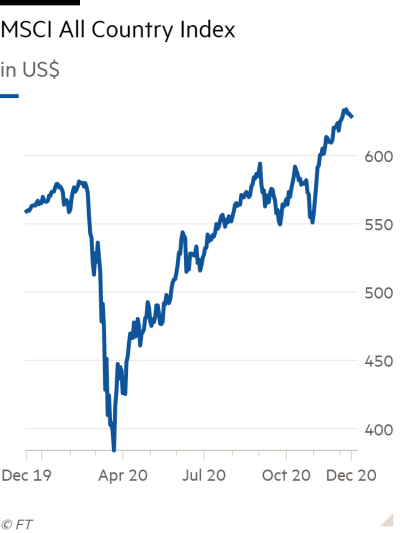

For most of us, the stunning rout in equity markets in the 1st quarter was more difficult to endure than those in 1987, 1990, or 2008 because of the risk to life in addition to wealth. Yet, shockingly, it only took a few months for stock prices to recover and show positive returns for the year. This in turn may legitimately raise concerns that markets are already pricing in more than the 2021 economic and earnings’ recoveries can provide.

In dealing with these wild market swings, our simple, time-tested strategies proved again to be effective: portfolio rebalancing, avoiding panic or euphoria, and paying attention to valuations. Committing to an investment plan provides a compass and makes it much easier to make decisions during challenging times. The period during March and April was the proverbial fork in the road: you either followed the dire forecasts and hit the exits running or stuck to your plan and took advantage of the opportunities available.

Logically, we were pro-active in seizing the moment: we rebalanced, where appropriate, our clients’ portfolios into stocks, stock funds, preferred securities, and other asset classes that had declined sharply. Depending on your personal situation, we also called and encouraged you to consider Roth conversions or add cash to your account and take advantage of depressed asset valuations. Clearly, our timing was not always perfect, and markets could easily have declined further, longer, or both. But if we don’t buy when assets are cheap, when do we?

To your credit, you—the real partners in our namesake—demonstrated once again that you value Bristlecone’s contrarian approach to investing. Indeed, we received positive feedback for navigating this crisis and no one panicked.

We will be reflecting on 2020 throughout our lifetimes: lives lost, time spent away from loved ones, high school or college graduations passed without celebrations, and specific industries and socioeconomic groups disproportionately impacted. Some of the pandemic’s effects will last.

However, a year from now, we think we'll be able to look back and say that 2021 was an improvement. Progress may not be enormous, but it will be a noticeable, measurable step forward for people worldwide.

The main reason to be hopeful is that in the spring of 2021, vaccination should start reaching the scale where it will have an impact. The number of cases and deaths should start to go down and life should return progressively to normal.

A Closer Look at the 4th Quarter

As mentioned earlier, stock markets worldwide saw very strong performance during the quarter with returns in double digits for every category. Interestingly, the laggards of the past few years finally beat the leaders across several equity segments: Value outperformed Growth, while International and U.S. Small-Cap outperformed U.S. Large-Cap stocks.

In contrast, the U.S. bond market struggled a bit. Prices declined and the yield from the benchmark 10-year U.S. Treasury is now just under 1% after dipping to a low of 0.5% during the crisis. Bond investors, like their equity colleagues, are anticipating an economic recovery in 2021, and possibly a small increase in inflation. It remains difficult to interpret the significance of price movements in the bond market, as the Federal Reserve continues to be proactive in keeping yields low. Reinforcing our view that some inflation pressure is building up, commodity prices also saw a double-digit increase. The table below illustrates a hypothetical 60/40 model portfolio allocation:

Anecdotal signs of speculative excesses appeared here and there: initial public offerings soaring on the first day, stories about day-traders’ quick fortunes, and the price of bitcoin finally breaking through its December 2017 high.

In the end though, 11 of the 13 asset categories represented in our clients’ portfolios—Real Estate and Commodities being the exceptions—achieved positive returns in 2020; the average balanced (i.e. holding both stocks and bonds) portfolio finished 2020 in the black, a remarkable result to close such a turbulent year (note: your portfolio’s allocation and results may differ—please refer to your Quarterly Portfolio Review Report).

Large Cap Value (LCV) Review

(Not all clients of Bristlecone are invested in our Large Cap Value Equity portfolio strategy, depending on the size of the overall portfolio, and the client's objectives and constraints)

Net of fees, the average LCV portfolio produced a gain in the mid to high teens during the quarter and ended the year slightly up. Its 2020 performance lagged the S&P 500 but exceeded that of the Large Value peer group (as measured by the Morningstar Large Value index). The year was really a tale of two halves though: with Value and Small Cap stocks outperforming late in the year, the portfolio regained about a third of its 1st half relative underperformance. Despite these late positive signs, our commitment to a value philosophy continued to be tested.

If mean-reversion history is any guide though, the image of a stretched elastic band applies. Witness the steepness of the graph in 2000 (a rising line indicates value outperformance relative to growth, a declining line shows value underperformance): recoveries tend to happen fast. Value stocks still have a long way to go to make up for the relative underperformance of the past few years.

Not surprisingly, we were more active than usual in 2020. As the crisis unfolded from March through July, we were net buyers and put some cash to work. We made new investments in Apple (AAPL), and Howard Hughes (HHC). We also increased our holdings in Anheuser Bush (BUD), Graham Holdings (GHC), and Intel (INTC). Although all these purchases have worked out so far, there is no telling whether they will over the next 3 to 5 years.

In addition to the sale of Expedia (EXPE) discussed below, we liquidated our position in Aggreko (ARGKF). We also took advantage of the market recovery to reduce our investments in Pfizer (PFE) and Agco (AGCO). Worth noting too, our biggest holding, GCI Communication (GLIBA), was acquired by Liberty Broadband (this was a stock transaction, so we now own shares in LBRDK). Finally, we received shares in two spinoffs: Viatris (VTRS) and Qurate 8% Preferred (QRTEP).

Trying Not to Form Mental Chains

While it would be inappropriate to discuss stocks that we are in the process of buying, it is not uncommon for us to review specific investment decisions in our commentaries or over the phone. Although it can help clients understand our process and our thinking, we confess to having some reluctance— mostly due to psychology—to publicly lay out our rationale.

There are risks in trying to convince you of the merits of a specific investment. First, we do not like to appear promotional. More importantly, there is also a risk that we will convince ourselves to the point of compromising our objectivity. Would we remain totally open to changing our minds if new evidence that contradicted our case came to light just a few days after making it public? These self-imposed “mental chains” were highlighted by Charlie Munger in his famous 1995 speech at Harvard University, “The Psychology of Human Misjudgement”: “if you make a public disclosure of your conclusion, you’re pounding it into your own head.”

To illustrate, we chose to discuss a sale, Expedia (EXPE). As the pandemic hit, the stock price promptly dropped to an 8-year low in March. A few weeks later, after the stock price had recovered a bit, we sold our entire position at an average loss of about 50%.

We laid out the original case in our 4th quarter 2017 commentary. Our analysis revealed a potential investment that checked several boxes on our list: a market with excellent growth potential, high free cash flow yield, attractive economics, strong competitive position, quality balance sheet, and reasonable valuation. Analyzing these issues as objectively as possible to make better investment decisions is within our control.

However, with investing, other important factors remain out of our control: managers make mistakes, companies respond inadequately to new competitive threats, share prices divorce from reality, economies suffer external shocks, and… pandemics all but shut down travel and tourism. As the CEO of a UK hotel and restaurant group noted in the Financial Times: “We thought we had a scenario for everything. It turned out we had no scenario for the complete closure of our business.”

We justified liquidating this investment in a subsequent commentary. Not surprisingly, our main concern was the impact that a dramatic drop in revenues would have on the company’s finances. We questioned Expedia’s ability to ride out the crisis without raising capital and diluting existing shareholders or, alternatively, going bankrupt.

Imagine that, instead of buying our original investment in November 2017, we had bought it in November 2019 and discussed our rationale in the commentary published in early 2020. How likely would we have been to liquidate the entire investment just a few weeks later? To deny that we would have second thoughts that could potentially affect our decision is likely naïve.

The final twist in the story is that Expedia’s share price is now much higher than when we sold it. With hindsight, inaction would have produced a better outcome… but our point about the process remains valid.

About that Soufflé

In 2020, the Candid Comment of the Year award goes to Tesla’s founder Elon Musk when discussing his firm’s share price gain and entry into the S&P 500: “When looking at our actual profitability, it is very low… Investors are giving us a lot of credit for future profitability, but if at any point they conclude that's not going to happen, our stock will immediately get crushed like a soufflé under a sledgehammer!”

On December 21, Tesla joined the S&P 500 Index, a widely used benchmark for the U.S. stock market. From its March low through the end of the year, Tesla’s share price saw an eightfold increase. Most of that run-up occurred after the media began speculating about Tesla’s likely addition to the index. The rise has been meteoric:

Tesla is the largest stock to enter the S&P 500 in the index's history by rank (6th) and absolute market capitalization ($678 billion as we write this note). By the close of trading on December 21, index funds, ETFs, and other index-tracking strategies had to own $70 billion worth of Tesla shares.

Tesla is an impressive and influential company in the electric vehicle space. The company has a well-regarded brand and first-mover advantage in a fast-growing market segment. Yet it is far from the only player in its industry: existing automakers already produce more than twice as many electric vehicles as Tesla and have plans to invest tens of billions of dollars in bringing new ones to market.

According to Research Affiliates (chart below), the top nine automakers, whose combined market capitalization is below that of Tesla, produce 121 times as many cars. Yet, Tesla is priced at a higher valuation (“only” $608 billion at the time).

The company’s inclusion serves as a useful reminder that the S&P 500 is not a true passive representation of the U.S. stock market. Its components are selected by a committee from S&P Dow Jones Indices (in an unrelated incident, an employee just pleaded guilty to tipping friends on index changes in December).

By owning a fund that tracks the S&P 500, investors are delegating management to a group of people who are using both subjective and quantitative criteria. As Howard Marks of Oaktree Capital stated: “somebody is making very active decisions about which stocks will be in each ‘passive’ product. […] the people who create the indexes are deciding which stocks will be invested in”.

We are big fans and frequent investors in index funds within our asset allocation process. This is due to their low expenses, tax efficiency, and ability to set a performance benchmark for a specific market segment in one easy-to-invest instrument. At the same time, we understand their limitations and shortcomings. There are enough examples of construction issues to give us pause at times.

Within the last few years, we have regularly pointed out in our commentaries that the S&P 500 has become less diversified and more concentrated in its top holdings. We are concerned that it might not track the U.S. economy or the stock market’s broader performance in years to come. From a valuation standpoint, other segments appear more attractive as well. We would rather heed Musk’s warning than implicitly buy shares in Tesla at their current market appraisal.

Clueless About 2021

Each December, Wall Street strategists like to predict the stock market’s performance for the coming year. The median forecast very rarely calls for a decline. Yet, history shows that the odds are about 25% to 30%.

Predicting what the market will do in the short-term is a waste of time. It only matters whether one realizes it or not. It is also extremely hazardous to your wealth. Here’s the performance cost of missing the best trading days (out of a total of about 250) in the market every year for the 20-year period from 1999 through 2018:

In conclusion, we’re back to where we started: no matter what 2021 brings, we will stick to the same simple, time-tested strategies: portfolio rebalancing, avoiding panic or euphoria, and paying attention to valuations.

After the year we just had, we want to especially thank each one of you for the trust and confidence you place in all of us at Bristlecone Value Partners.

We wish you, and your families a safe and happy 2021.

One of Bristlecone Value Partners’ principles is to communicate frequently, openly, and honestly. We believe that our clients benefit from understanding our investment philosophy and process. Our views and opinions regarding investment prospects are "forward-looking statements," which may or may not be accurate over the long term. While we believe we have a reasonable basis for our appraisals, and we have confidence in our opinions, actual results may differ materially from those we anticipate. Information provided in this blog should not be considered as a recommendation to purchase or sell any particular security. You can identify forward-looking statements by words like "believe," "expect," "anticipate," or similar expressions when discussing particular portfolio holdings. We cannot assure future results and achievements. You should not place undue reliance on forward-looking statements, which speak only as of the date of the blog entry. We disclaim any obligation to update or alter any forward-looking statements, whether as a result of new information, future events, or otherwise. Our comments are intended to reflect trading activity in a mature, unrestricted portfolio and might not be representative of actual activity in all portfolios. Portfolio holdings are subject to change without notice. Current and future performance may be lower or higher than the performance quoted in this blog.

References to indexes and benchmarks are hypothetical illustrations of aggregate returns and do not reflect the performance of any actual investment. Investors cannot invest in an index and returns do not reflect the deduction of advisory fees or other trading expenses. There can be no assurance that current investments will be profitable. Actual realized returns will depend on, among other factors, the value of assets and market conditions at the time of disposition, any related transaction costs, and the timing of the purchase.

Economic factors, market conditions, and investment strategies will affect the performance of any portfolio and there can be no assurance that a portfolio will match or outperform any particular index or benchmark. Past performance is not indicative of future results. All investment strategies have the potential for profit or loss; changes in investment strategies, contributions, or withdrawals may materially alter the performance and results of a portfolio. Different types of investments involve varying degrees of risk, and there can be no assurance that any specific investment will be suitable or profitable for a client's investment portfolio.

This content is developed from sources believed to be providing accurate information, and it may not be used for the purpose of avoiding any federal tax penalties. Please consult legal or tax professionals for specific information regarding your individual situation. The opinions expressed and material provided are for general information, and should not be considered a solicitation for the purchase or sale of any security.